Ray Geiger/iStock Editorial via Getty Images

The Buy Thesis

Postal Realty (PSTL) is substantially undervalued relative to its growth rate and the cleanliness of its business model. I believe the stability of Postal is overlooked due to the lack of analytical coverage on the niche in which PSTL operates. I think the actual business fundamentals warrant a substantially higher AFFO multiple (18X), equating to a stock price about 50% above the current market price ($23.58 versus the current $15.36).

We shall begin with a conjecture as to why PSTL is trading at such a low multiple and follow with fundamental analysis, which we believe supports the 18X multiple.

Why PSTL’s multiple is 11X

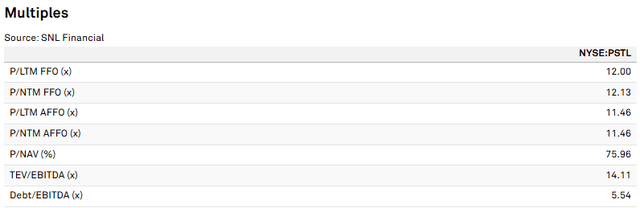

As of 11/6/25, Postal is trading at the following valuation multiples.

S&P Global Market Intelligence

The 76% of Net Asset Value indicates PSTL is trading substantially below the value of its underlying properties.

An 11X forward AFFO multiple is typical of REITs that have one of the following problems:

·Low or 0 growth

·High risk

·High debt

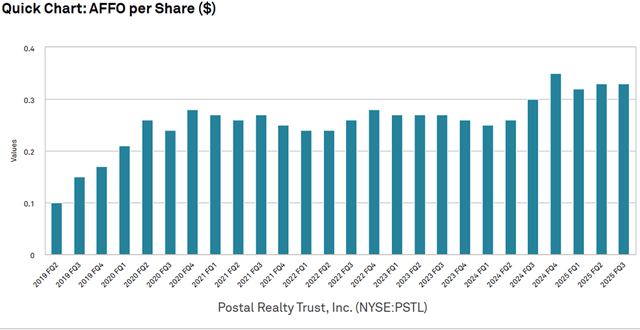

Postal does not fit that profile at all. AFFO/share growth since 2021 has been just over 8% annually.

S&P Global Market Intelligence

An ~8% AFFO/share growth rate would normally be associated with an AFFO multiple of about 20X.

Further, analysis of its business model and balance sheet suggests it is neither high risk nor high debt.

So why is PSTL trading so cheaply?

The short answer is obscurity. PSTL has a float of just under $400 million and is the only publicly traded company operating in its niche (post offices leased to USPS).

That is far too small for most large institutions to invest in it. It is these large institutions that would have the analytical power to do dedicated research on individual companies.

Smaller investors, both professional and retail, tend to operate and develop expertise in certain sectors. If a new senior housing REIT IPOs, it is quite easy for those who already study Ventas (VTR) or Welltower (WELL) to pick up and understand the new SH REIT.

With no public peers and no public predecessors, there was no natural audience for PSTL. The physical properties are a mix of industrial and office, but the fundamentals of post office leasing are drastically different than those of either sector.

As such, pre-existing investment knowledge does not transfer in well. One has to study Postal Realty specifically, and few dedicate that much time to individual, niche, small cap stocks.

We at 2nd Market Capital specialize in overlooked stocks. There are many landmines in the obscure small-cap space, but we believe Postal Realty is a diamond in the rough.

I think the multiple at which it trades is a consequence of obscurity being misinterpreted as risk. Specifically, there are 4 judgments that I think the market is getting wrong.

4 Bear Arguments:

·Very small size

·Uncertainty of lease renewal timings and conditions

·Unproven asset class

·Uncertain pipeline

Each of these has been largely proven wrong.

Postal is indeed small, with a $400 million float and a total market cap inclusive of OP units of $509 million. In a world dominated by multi-trillion-dollar Magnificent 7 companies, Postal Realty appears to be subscale.

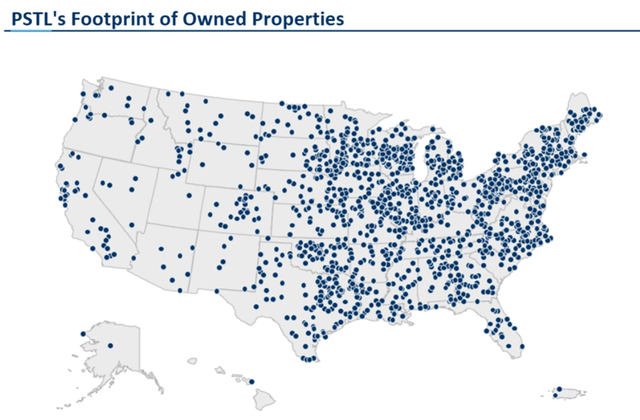

However, within its niche, Postal is the 800-pound gorilla in the room. They have a dominant market share in post office real estate (greater than 10% of TAM). They dwarf their next largest competitor, with the majority of owners being Mom and Pop types of owners that have 1-5 buildings. PSTL’s portfolio spans the entire U.S., and they are the go-to for anyone looking to sell postal real estate.

PSTL

I think there has been quite a bit of apprehension regarding lease rollover. Historically, the government has been slow to sign new leases, only executing in batches, causing some to even incur back pay as the new leases are sometimes signed well after expiry.

In any other kind of real estate, an expired lease that is not yet re-leased can be very bad news.

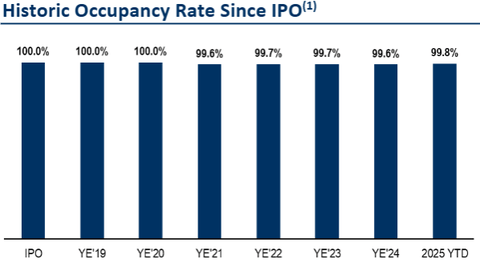

However, leases with the USPS are different. They overwhelmingly turn out just fine with extraordinarily high renewal rates leading to unmatched occupancy levels.

PSTL

PSTL has also made great improvements in the lease negotiation process. It is now faster, more streamlined, and includes terms that are quite favorable to PSTL investors.

Andrew Spodek (CEO of PSTL) described leasing negotiations on the 3Q25 earnings call:

“Starting with leasing, we have worked with the Postal Service to create a highly efficient and repeatable framework to negotiate, process and execute new leases across both our existing portfolio and future acquisitions. This approach has yielded important benefits for both parties.

For Postal Realty, this framework has improved the predictability of our long-term revenue growth with our new leases offering a mix of 10-year term and 3% annual rent escalations. We are also now able to anticipate rental rate timing and ranges for future lease commencements further in advance than ever before.”

He went on to specify how the better leasing translates to net operating income (NOI):

“Based on our success advancing our new leasing approach and driving property operating efficiencies, we are updating our 2025 same-store cash NOI guidance to a range of 8.5% to 9.5% from our prior guidance of 7% to 9%.”

High NOI growth with strong escalators and nearly 100% renewal rates is superior leasing to just about any other kind of real estate.

Post offices as an asset class have also been viewed with anxiety.

·As Presidential administrations changed, people feared a restructuring.

·DOGE (Department of Government Efficiency) was anticipated to potentially cut the USPS budget.

·The ongoing government shutdown has been viewed as a potential risk to anything government funded.

None of these risks manifested in any fundamental harm to Postal’s leasing. PSTL has 100% rent collection and consistently grows rental income.

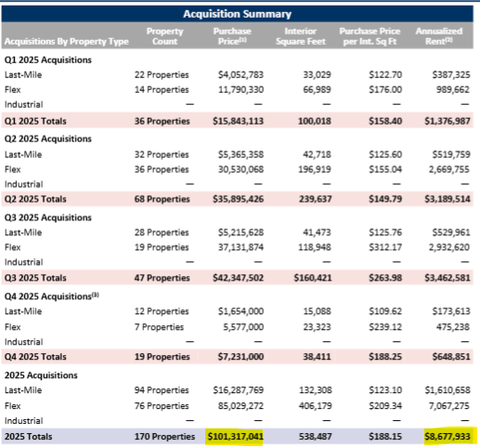

Finally, there has been worry that Postal would be limited in its growth as it operates in such a small niche. However, year after year, PSTL has been able to source healthy acquisition volumes. In 2025, they put together over $100 million of acquisitions.

PSTL

For a $500 million market cap company, that is a massive pipeline.

As time goes on, the bear explanations for PSTL’s low AFFO multiple are getting increasingly weaker.

Fundamental Support For Higher AFFO Multiple

There are 3 aspects of Postal’s business that we believe warrant a higher multiple of about 18X AFFO.

1)AFFO/share growth rate

2)Clean business model

3)Clean balance sheet

AFFO/Share Growth

We already touched on Postal’s historical growth rate of about 8% annually. The company is well positioned to maintain a similar growth rate going forward.

3% escalators on new leases provide a solid baseline growth rate.

Acquisitions produce the rest. As discussed above, PSTL sourced over $100 million of acquisitions in 2025. These acquisitions come with excellent spreads over cost of capital. Acquisition cap rates are in the high 7s, with the most recent quarter’s coming in at 7.7%.

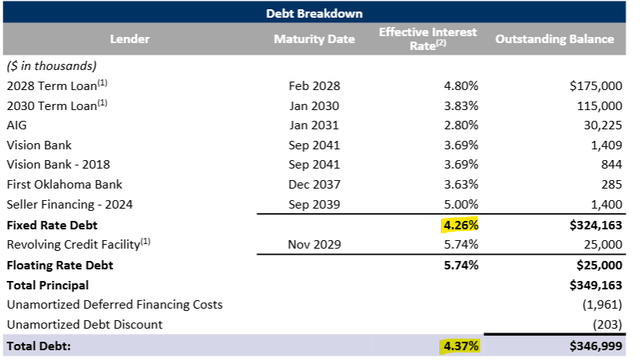

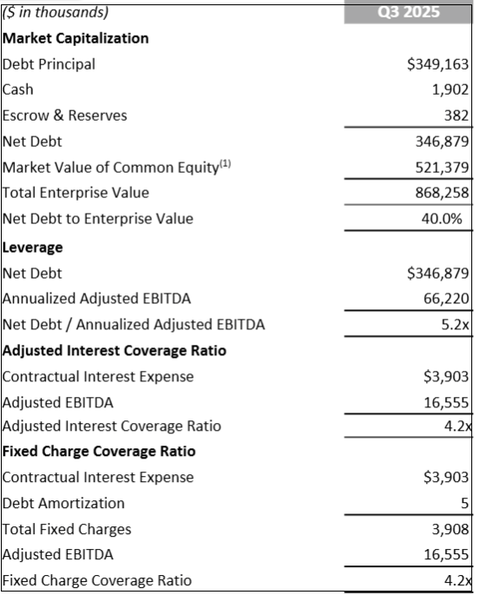

Cost of debt is rather low for Postal, as their balance sheet sits at 5.2X debt to EBITDA and 4.2X fixed charge coverage ratio. These favorable metrics sit well with creditors, allowing PSTL to maintain an average cost of debt of 4.37%.

PSTL

Equity is somewhat expensive for Postal presently due to the low AFFO multiple. Issuance at current market pricing costs about 9% on a dilutive basis.

However, as an UPREIT, Postal can buy properties with OP units, and property sellers are often willing to take OP units at above market price because of the tax advantages they come with.

Since most sellers of post office properties are mom and pop owners who have owned the properties for a long time, their cost basis has depreciated to near $0, and selling would trigger a large capital gains tax.

But if they sell to PSTL instead, they can do a 721 exchange for OP units instead of cash. These OP units allow the property seller to defer taxation indefinitely as long as the shares are held.

With use of OP units, PSTL has a blended cost of capital somewhere between 6% and 7%, affording a healthy spread on acquisitions.

Clean Business Model

Triple net real estate is usually a clean business model. The REIT collects revenue net of most expenses, making for very high margins. Postal is no exception.

Supplemental

However, one of the challenges of triple net is upon lease renewal. Finding a new tenant usually incurs capex in the form of tenant improvement costs and leasing commissions.

For offices, these expenses are as much as 20% of revenue. For industrial, it is usually closer to 6%-8%.

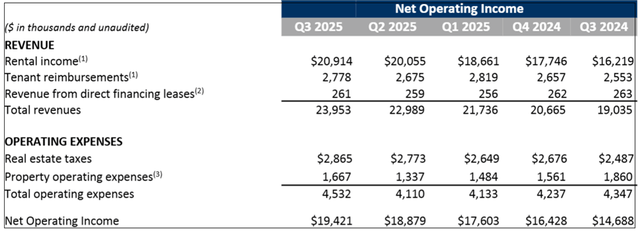

Since PSTL is re-leasing to the same government entity, much of the leasing expense can be avoided. Recurring capex for Postal was only 1.1% of revenue in 3Q25, and that number appears fairly typical for them.

Overall, post office real estate seems to be a clean, recurring revenue stream with a good amount of organic growth.

Balance Sheet

We touched on some of these metrics in discussing the cost of debt earlier, but PSTL’s debt is surprisingly good for a small cap REIT.

Supplemental

Maturities are well laddered too.

Summary Of Buy Thesis

Given the strong business model, clean balance sheet, and relatively high growth, I believe Postal should trade at about 18X AFFO. 2025 AFFO is estimated at $1.31, which implies a fair value of $23.58. I don’t see fundamental justification for the very low multiple at which PSTL currently trades. I think the stock price will rise over time as more successful quarters bring public perception of PSTL from obscure to tenured.

Risks

The main risk to PSTL is its extreme tenant concentration, as it has close to all of its NOI from a single entity.

In my opinion, the U.S. government is an excellent tenant, but this level of concentration creates the potential for a calamitous NOI loss if the government’s views on the necessity of postal service were to suddenly shift.

This risk can be mitigated by proper diversification in an investor’s portfolio. While PSTL is concentrated, it is the only post office exposure in my portfolio, making changes to USPS only affect a modest portion of my holdings.

seekingalpha.com (Article Sourced Website)

#Postal #Realty #Stock #High #Growth #Cheap #Multiple #NYSEPSTL